通知公告

首页»

通知公告

通知公告

04.20 金融系Seminar:Beta Reversal and Expected Returns

发布时间:2015-04-10

浏览量:

题目:Beta Reversal and Expected Returns

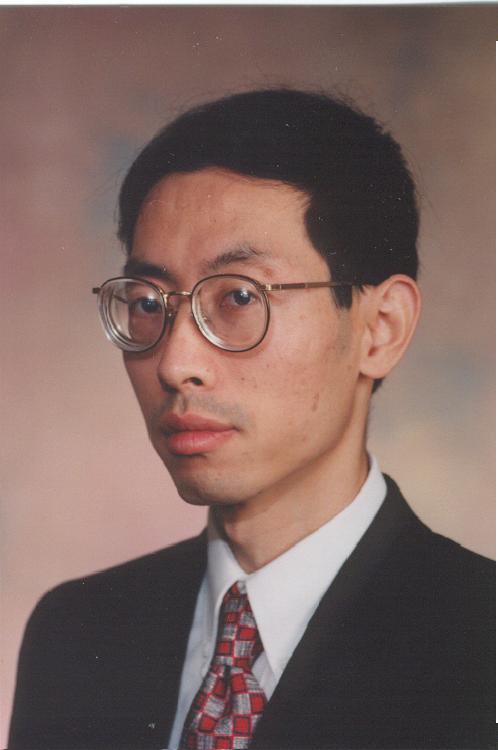

嘉宾:Associate Professor Yexiao Xu,Naveen Jindal School of Management,The University of Texas at Dallas

时间:2015年4月20日(周一) 9:30 - 11:00

地点:后主楼1722室

嘉宾简介:

Professor Yexiao Xu received his Ph.D degree in financial economics from Princeton University in 1996. Currently he is an associate professor in the School of Management, the University of Texas at Dallas. He has won the 2001 Smith-Breeden prize for a study on idiosyncratic risks—one of the most prestigious awards in Finance. His published and working paper have generated over 3,600 citations. Professor Xu’s research interest covers stock market volatility, the pricing role of idiosyncratic risk, factor models, predictability, mutual fund performance, analyst research, tax and close-end fund discounts, and adaptive estimators. Currently he is working on a number of topics including asset pricing test, implied cost of capital, predictability of idiosyncratic risk, partial factor structure, economic models for leverage, short sale interest, and many related issues in the Chinese and Japanese equity markets. Professor Xu has taught Ph.D. level theoretical and empirical asset pricing courses, financial economics, as well as MBA financial management and investment courses.

内容摘要:

In this paper we show that it is the beta reversal among a small group of stocks that prevents the CAPM beta from predicting individual stocks’ expected returns as documented by Fama and French (1992). These stocks tend to have both large beta and high idiosyncratic volatility. Consequently, even when the CAPM holds period-by-period, the confounding effect of beta reversal diminishes the significance of the CAPM beta in the cross-sectional tests. The cross-sectional explanatory power of beta is restored after wetake into account the beta reversal effect in each of the three ways. More important, the market risk premium estimated from cross-sectional regression analysis is almost identical to the historical average of market excess returns. All results are robust with respect to different measures of beta and idiosyncratic volatility as well as different subsamples. We also find that beta reversal is likely to be a result of several factors including the wealth effect, earnings announcement effect, and real option realization.

附件下载:

嘉宾:Associate Professor Yexiao Xu,Naveen Jindal School of Management,The University of Texas at Dallas

时间:2015年4月20日(周一) 9:30 - 11:00

地点:后主楼1722室

嘉宾简介:

Professor Yexiao Xu received his Ph.D degree in financial economics from Princeton University in 1996. Currently he is an associate professor in the School of Management, the University of Texas at Dallas. He has won the 2001 Smith-Breeden prize for a study on idiosyncratic risks—one of the most prestigious awards in Finance. His published and working paper have generated over 3,600 citations. Professor Xu’s research interest covers stock market volatility, the pricing role of idiosyncratic risk, factor models, predictability, mutual fund performance, analyst research, tax and close-end fund discounts, and adaptive estimators. Currently he is working on a number of topics including asset pricing test, implied cost of capital, predictability of idiosyncratic risk, partial factor structure, economic models for leverage, short sale interest, and many related issues in the Chinese and Japanese equity markets. Professor Xu has taught Ph.D. level theoretical and empirical asset pricing courses, financial economics, as well as MBA financial management and investment courses.

内容摘要:

In this paper we show that it is the beta reversal among a small group of stocks that prevents the CAPM beta from predicting individual stocks’ expected returns as documented by Fama and French (1992). These stocks tend to have both large beta and high idiosyncratic volatility. Consequently, even when the CAPM holds period-by-period, the confounding effect of beta reversal diminishes the significance of the CAPM beta in the cross-sectional tests. The cross-sectional explanatory power of beta is restored after wetake into account the beta reversal effect in each of the three ways. More important, the market risk premium estimated from cross-sectional regression analysis is almost identical to the historical average of market excess returns. All results are robust with respect to different measures of beta and idiosyncratic volatility as well as different subsamples. We also find that beta reversal is likely to be a result of several factors including the wealth effect, earnings announcement effect, and real option realization.

附件下载: